All about WorkCover impairment claims in Victoria

An impairment claim, sometimes referred to as a claim for impairment benefits or impairment benefits claim, is open to someone to pursue if they have a work related injury or illness that has resulted in permanent impairment.

An impairment benefit is considered to be compensation for pain and suffering.

Table of Contents

How do I make an impairment claim?

In order to make an impairment claim you need to complete the appropriate claim form.

(In general, we recommend that people have a lawyer help them with an impairment claim).

You can get a blank copy of the impairment claim form here. You can also get a copy of this form from WorkCover insurer’s as well as WorkSafe.

Here’s what the form looks like:

Tips for filling out the impairment claim form:

When completing the claim form you will need to include your details, your employment details, the nature of the injury and how it happened.

When listing what the injury is, you need to ensure to list all relevant injuries and consequences of any injuries.

Here’s an example of consequence of an injury:

Let’s say that you suffered an injury to your shoulder and that as a consequence of the injury you need to take medication on a regular basis.

As a result of taking medication you have suffered stomach problems problems for which you now need to obtain treatment.

You should list, in addition to your shoulder injury, your stomach problems on the claim form.

When describing how the injury happened, you do not need to go into a lot of detail.

It’s sufficient to just say, for example, that you were injured while working on a particular piece of machinery. Or from repetitive lifting.

Remember, you do not need to prove fault in relation to this claim.

Also make sure to list any relevant previous injuries you may have had.

What happens once I’ve completed the claim form?

The claim form must be given to your employer.

They must then provide a copy of the claim form to the WorkCover Insurer.

The WorkCover insurer will then process your claim.

They will organise an appointment for you to be assessed by an independent medical examiner or more than one if you require doctors with different specialities to assess all of your claimed injuries. This is called an impairment assessment.

You can read more about independent medical examiner’s here.

Any injuries or conditions will then be graded by the specialist doctors. They’ll put percentage figures on them.

These percentage figures will then get combined into one overall figure.

What are the impairment threshold figures?

The overall figure must then reach a threshold level of impairment in order for you to succeed.

In order to be compensable, the whole person impairment rating for a physical injury has to be at least 10%.

If the injury is a musculoskeletal injury (eg: injury to your spine) then it must be 5% or greater.

For a psychiatric injury, you must be assessed as having 30% whole person impairment or greater.

This page explains whole person impairment further.

Can I organise my own doctors to assess me?

Your injuries need to be graded by specialist doctors that have undergone certain training which allows them to grade injuries in legal matters.

You are not able to have your own treating medical practitioners, including any specialist that you’ve seen, grade your injuries.

The doctors that can assess you must have training in the American Medical Association Guides to Permanent Impairment (this is a big red book referred to as the AMA guides).

Once the doctors have completed their assessments, their reports are sent to the insurance company.

The insurance company will consider the reports and then send out to your notice with an offer to resolve your impairment benefit claim.

This will include the whole person impairment rating and a corresponding compensation amount.

If you are happy with the whole person impairment rating and corresponding compensation amount, you can accept the offer from the insurance company and resolve your impairment claim.

Your matter will then be finalised and you should be paid your impairment benefit amount within about two to three weeks.

If you’re not happy with the offer that the insurance company has made you, that it is possible to appeal the assessment or assessments the medical panel.

Further information on the medical panel and what is involved, is discussed in length here.

Permanent impairment payout amounts in Victoria

Below are the permanent impairment payout amounts with relevant percentage figures, for claims in Victoria.

The actual tables are more detailed than these.

These tables only include compensation amounts relating to claims lodged in 2020/21.

If your claim was lodged before this period, then keep in mind that the compensation figure won’t be to the dollar accurate, but the actual amount you receive should be within this range (within a few thousand dollars).

Copyright – this is original content from theworkinjurysite.com.au.

To use the tables below to calculate your permanent impairment payout amount, first you need to ensure you select the right table.

Then, find the correct impairment percentage, which will correspond to a permanent impairment payout amount.

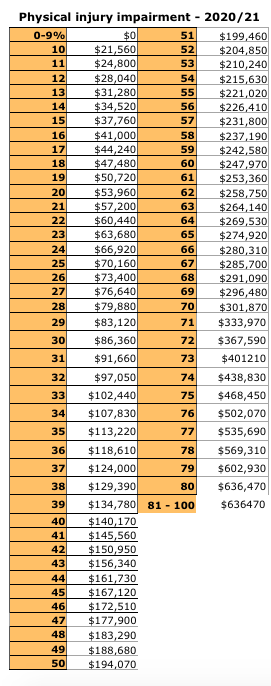

Permanent impairment table – physical injury:

Permanent impairment table – ‘chapter 3’ spinal impairments:

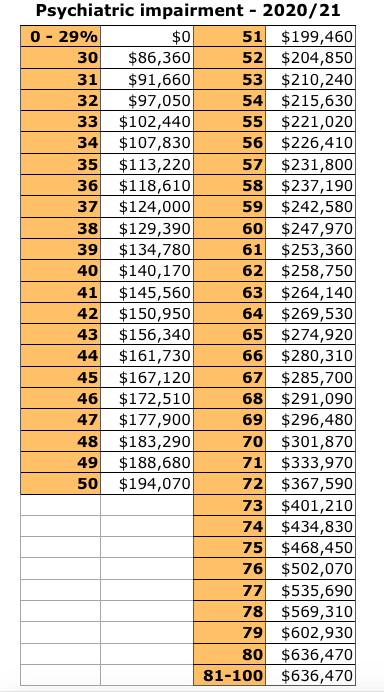

Permanent impairment table – psychiatric injury:

Is an impairment claim subject to tax?

No, an impairment claim is considered to be compensation for pain and suffering and is not subject to tax.

How long does an impairment claim take?

Generally speaking, a claim for impairment benefits can take about two to four months to finalise.

Sometimes it can take longer depending upon the nature of your injuries, the number of assessments that you need to undergo and the availability of doctors.

Also if further material needs to be requested to clarify a medical issue (eg: like an x ray or MRI scan) this can add to the length of time.

How is an impairment claim finalised?

An impairment claim is finalised once you have signed and returned the worker’s response form and elected to finalise the claim.

Alternatively, a claim is finalised if you fail to reach the minimum threshold level of impairment required after pursuing the matter to the medical panel.

Is court required in an impairment claim?

Generally speaking, court is not required. The only time you may end up in court relating to an impairment claim is if the insurer rejects liability for an injury and you wish to contest that decision.

Or if your matter progresses to the medical panel and you wish to appeal the decision of the panel.

Very few matters go to court that relate to impairment benefits.

Does an impairment benefit impact my other WorkCover entitlements?

An impairment benefit will not impact your entitlement to weekly payments or medical and like expenses in any way.

In relation to a common law claim, anything that you receive by way of an impairment benefit will be taken into account when it comes time to resolve your common law matter.

This is because an impairment benefit is considered to be compensation for pain and suffering, and part of what you’re being compensated for in a common law claim is also pain and suffering.

Do I have to pursue an impairment claim if I’m intending to pursue a common law claim?

As mentioned above, anything you get by way of an impairment claim is taken into account if you are successful in a common law claim.

For this reason, in some cases it can make sense to skip the lodgement of an impairment benefit claim and go straight to a common law claim.

If you pursue a common law claim and you are not successful, you can pursue an impairment benefit claim then.

However, this is a decision that should be made with the assistance of someone with experience in the WorkCover scheme and we would suggest that you speak to a lawyer for advice in relation of this.

Do I need to prove fault to claim to make a WorkCover impairment claim?

It doesn’t matter whether someone else was at fault for the injury or illness or not.

Anyone that is injured at work is able to pursue a claim for impairment benefits. You do not need to prove that another party was negligent.

How long after suffering my injury can I lodge an impairment claim?

In order to lodge an impairment claim your injury needs to be stable.

That means that it has played out. It is not getting any better and it is not getting any worse.

This is because you are getting compensated for any permanent impairment that you may have and so in order to do so, your injury needs to be given time to stabilise.

A general guideline as to how long it takes for an injury to stabilise is 12 months from the date of injury.

However, stability depends really upon the nature of the injury as some injuries can be stable much quicker than this while others can take a longer period of time.

Also, if surgery is on the cards in the short term, you need to wait until you’ve had the surgery and recovered from the surgery before your injury can be considered stable.

Can I choose the IME that assesses my injury?

No, the insurance company is responsible for selecting the doctor that assesses your injury.

If however you have seen the doctor before, say earlier on in the life of your WorkCover claim, you are not able to see this doctor again.

If this is applicable to you, then we would suggest letting the insurance company know.

Can I lodge more than one impairment claim for an injury?

No, you are able to lodge one impairment claim only for an injury.

If you have a hearing loss claim, you are able to lodge two impairment claims if you can show that you have suffered further hearing loss since your previous impairment claim resolved.

Considering weekly payments when deciding to lodge an impairment claim

In order for an injured person to remain on weekly payments post 130 weeks, if their 130 week mark occurs on or after 31 March 2024, they must have a 21% or greater whole person impairment rating.

This is in addition to the requirement that they you have no current work capacity, which is likely to continue indefinitely.

There is the possibility that if you go through the impairment benefit process and are assessed as having a 20% or less impairment, that it will cause the insurer to, or make it more likely that the insurer does, terminate your payments at the 130-week mark.

It may have been that if there was no 20% or less impairment rating through the impairment process that you would stay on payments for longer, as the insurer may not have you medically assessed for the purposes of weekly payments.

It is entirely a matter for you as to whether you proceed with an impairment claim or await a decision on your weekly payments at 130 weeks.

However it is our opinion that, generally speaking, that if there is some prospect of you remaining on weekly payments, that you do not lodge an impairment claim until a decision is made by the insurer at 130 weeks.

As the changes to weekly payments have only recently come into effect at the time of writing, it is uncertain how WorkSafe and their authorised insurers will deal with these issues.

For example, it is unclear as to how strict they will be on having people assessed for 21% or greater whole person impairment as there is to our knowledge currently, no set procedure in place.

If you are being certified as having some capacity for work, then your weekly payments will very likely be terminated based upon that capacity, and the questions concerning 21% whole person impairment or greater will not matter and there will be no issue with lodging your impairment claim.

And of course, if you’re not in receipt of weekly payments (and you don’t have an entitlement to weekly payments) then this section doesn’t apply to you.

Impairment benefit case study 1:

Robert suffered injury to his back during the course of his employment with a timber mill.

The injury occurred as a consequence of working on a particular piece of machinery and having to manoeuvre heavy logs from time to time.

He lodged an initial WorkCover claim which was accepted without issue. He required a few weeks off work and then returned to work on a gradual basis. After a few months, he returned to work working his full pre-injury hours, but on modified duties.

After about eight months post injury, he underwent surgery to his back.

Twelve months later, his doctors determined that his back injury had stabilised.

At this point, Robert elected to lodge an impairment benefit claim.

He completed the claim form with his lawyer, and this was sent off to his employer.

The insurer then organised an assessment for Robert to be seen by an orthopaedic surgeon.

About six weeks after the claim was lodged, Robert attended the appointment with the orthopaedic surgeon.

The assessment lasted about 30 minutes with the orthopaedic surgeon performing a number of tests.

After three weeks, Robert received correspondence from the insurance company with an offer to resolve his impairment benefit claim. It advised him that he had been assessed as having whole person impairment rating of 10% and that he was entitled to a lump sum payment of approximately $24,000.

After discussing the matter with his solicitor, Robert agreed to accept this offer and to not appeal the matter to the medical panel.

Robert signed a document accepting the offer.

About two weeks after signing the document, Robert received payment into his account.

Impairment benefit case study 2:

Jenny suffered injury to her right shoulder during the course of her employment as a personal care attendant.

There was no specific incident that caused the injury, but rather it occurred as a result of her duties over time.

She lodged a WorkCover claim which was accepted without issue.

She had some medical treatment on her shoulder but did not require surgery.

About twelve months after lodging the initial WorkCover claim, she lodged an impairment benefit claim.

She was assessed as having a 9% whole person impairment rating.

After considering the assessment and the nature of her injury, she elected to proceed to the medical panel.

She attended the medical panel about four weeks after she saw the independent medical examiner.

After an assessment from the panel, she received notification that the panel had increased the whole person impairment rating of 9% to 12%, which entitled her to gross payment of approximately $28,000.

She elected to accept the offer and resolve her impairment benefit claim.

Further reading:

If you would like to see more WorkCover compensation examples visit this page.